Comparing the prices of stocks across national borders is not like comparing the price of a liter of gasoline from one country to the next. The price of a stock is or really should be the present value of the future stream of earnings of that company. The ratio of the price of a common stock to either its historical earnings or expected earnings, its “PE Ratio”, is a reasonable way to compare stock prices across borders.

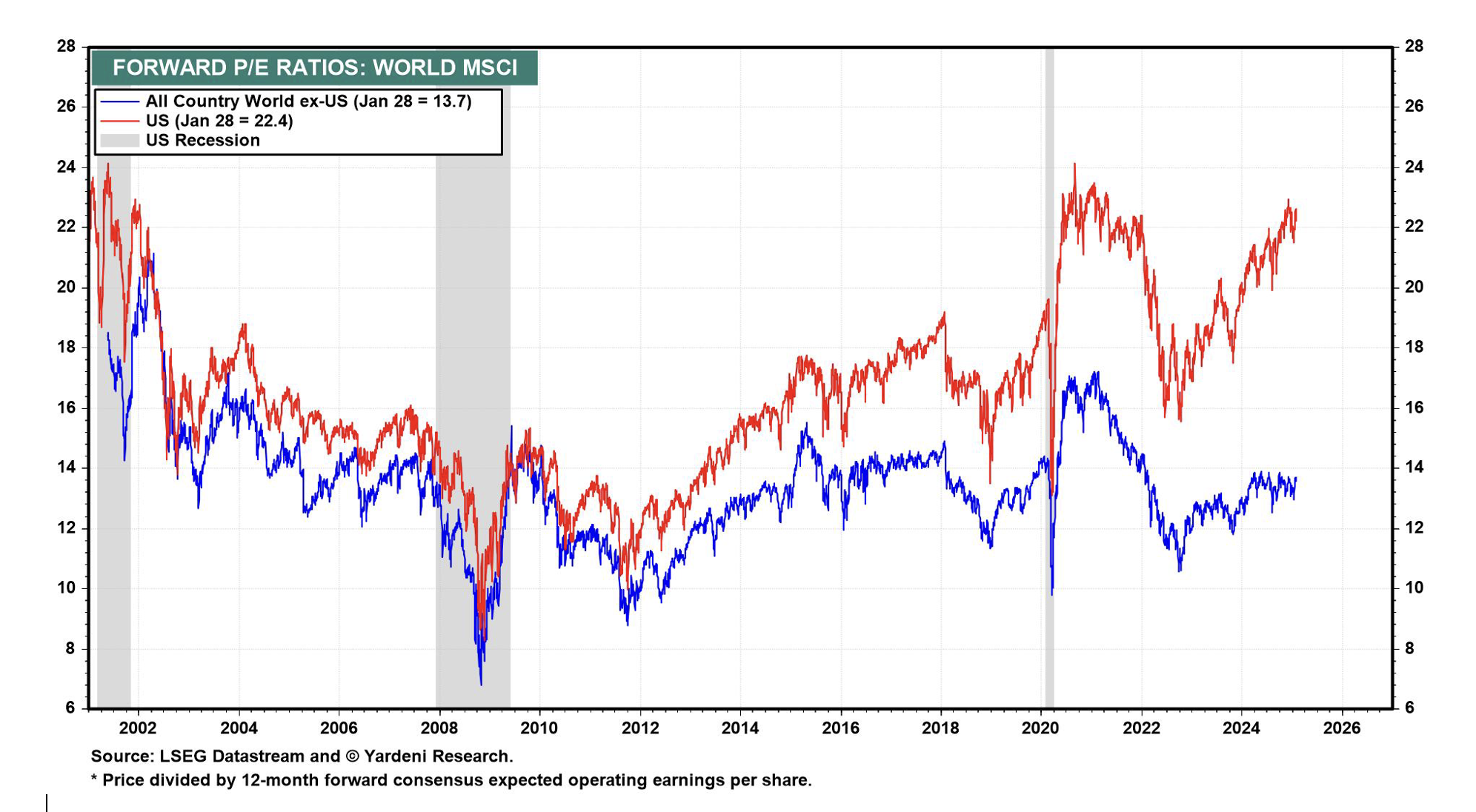

What is the level of this “price/earnings ratio” in the US and how does it compare to other countries? The table above shows that the average US equity is selling at a PE ratio of over 22 times forward (or expected) earnings as compared to an average multiple below 15 for the rest of the world. The multiple of US forward earnings of 22 is significantly higher than the average PE ratio in Japan at 14.5, Canada at 15.7, and Germany at 14.

What explains this exceptional valuation? In the following, we offer two explanations. One describes a popular rationale today and the other a more statistical explanation.

AMERICAN “EXCEPTIONALISM”

It was Alexis de Tocqueville who first described America as exceptional …in 1831. This ancient and very French description of the United States was almost forgotten by history for a hundred years, coming into common use again in the late 1920’s. Now almost another century later, that usage is popular again, including being featured in Donald Trump’s inaugural address. “America will soon be greater, stronger and far more exceptional than ever before.” 1/20/25

Some linguists contend that the meaning is only that America is unique, thinking that exceptionalism is really a synonym for uniqueness. Tocqueville meant that the United States was uncommon, special and beyond what was ordinary in the 1830’s. He noted the individualism that distinguished early nineteenth century America. It was the frontier spirit, the “rugged individualism”, and the “vibrant civil society” that he had observed. In many ways, these characteristics still survive today in America. These “animal spirits” seem to be alive and well again. Our system encourages risk-taking, and it does not punish failure as some other countries do. It’s no wonder that many want to come to the US and once they are here, stay here.

America has recorded growth rates coming out of the pandemic that have effectively carried the global economy, and the International Monetary Fund has projected future growth in the US at more than double the growth rate of our European allies. Some of this robust growth can be attributed to liquidity. The US has injected more money into the economy than most other nations. But admittedly, much of this growth can be attributed to the resurgence of the energy and spirit of its people. American exceptionalism is real, and it still does exist in the hearts and minds of its citizens.

A STATISTICAL REASON FOR HIGH US VALUATIONS

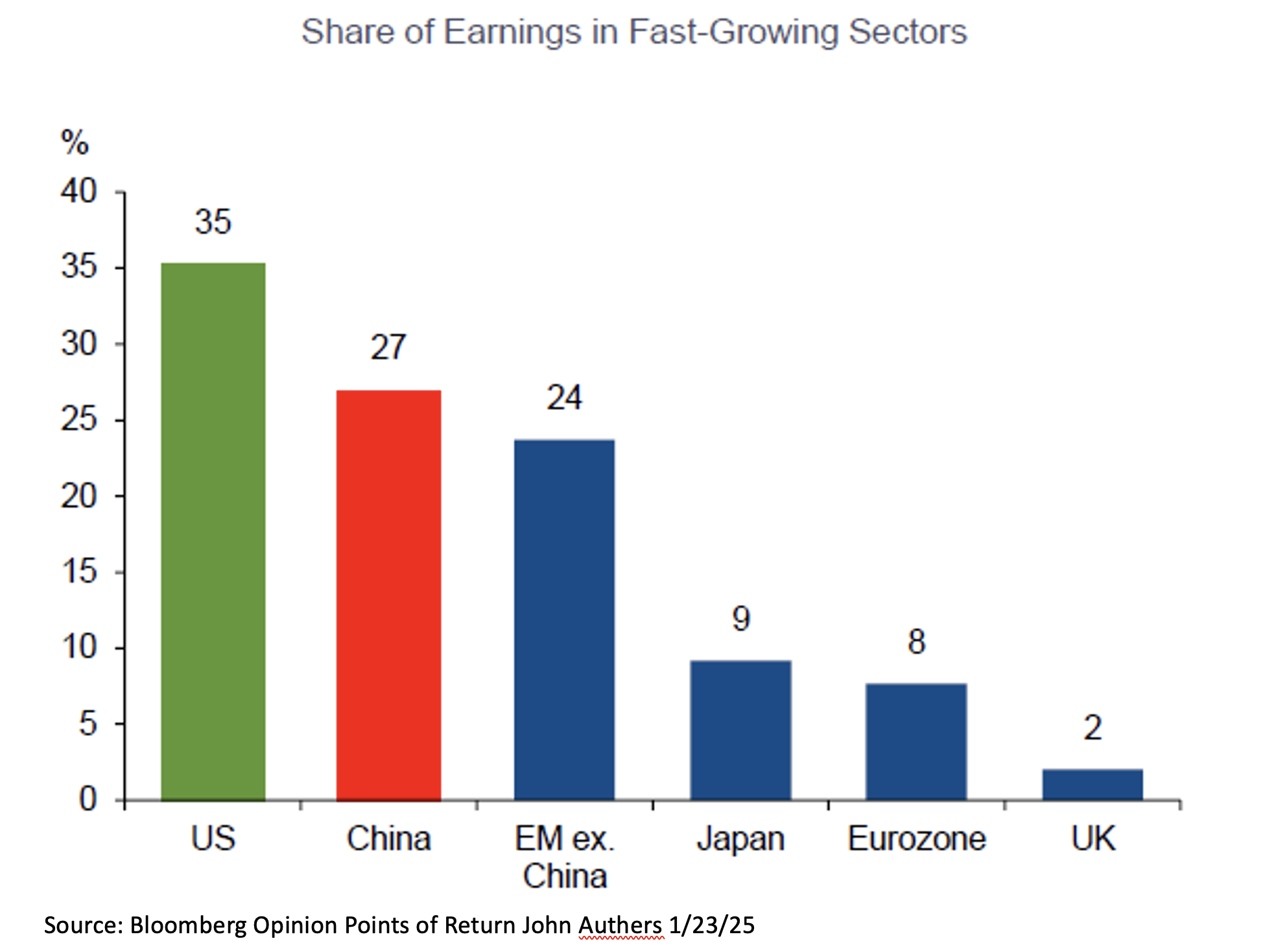

The US market is dominated by information technology and other technology-related, fast-growing companies, which historically have commanded higher price earnings ratios than the market.

IT companies have an average price/earnings ratio of close to 30 times forward earnings. The same is true for some of the other emerging economies like India. The chart below shows what may be a simple answer to the original question. American companies are valued higher because more American companies are in businesses where earnings are growing faster, thus warranting higher multiples. The explanation of American Exceptionalism may be true, and it certainly sounds good, but the real reason may be simply this. The higher valuation of US stocks is warranted, persistent and sustainable.

Sources

https://www.bloomberg.com/account/newsletters/points-of-return

Forward P/Es – Yardeni Research https://yardeni.com/charts/forward-p-es/

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed. The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results. We recommend that you compare our statement with the statement that you receive from your custodian. A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part 2A & Privacy Policy is available upon request or at www.baldwinmgt.com/disclosures.

Richard K. May, Managing Director (RKM), Business Development

Richard founded his financial advisory firm in 1980, which was one of the early fee-only advisors in the industry. He received his B.A. from Princeton University and his M.B.A. from the University of Michigan.

In 2007, Richard founded the West Chester LLC, a private equity company that promoted and funded business start-ups and public projects in the Borough of West Chester. In 2011, he co-founded the Uptown! Entertainment Alliance and the Uptown! Bravo Theatre, LLC. Together they purchased and rehabilitated the National Guard Armory, and then opened the Uptown! Knauer Performing Arts Center in 2016. Richard also serves on the board of Chester County OIC and is currently working on starting a live performance venue in Kennett Square, PA for 2025.