Soon after the most recent Federal Open Market Committee meeting – where the Fed’s Governors determine the level of interest rates (i.e., the Federal funds rate) – when the Fed paused its march of interest rate increases for the first time in months, Chairman Powell announced that the Fed was not done raising rates this year, even though that decision would be data dependent on future data. Huh?? We find it curious to pause, but to also assert that more is to come. Then Chair Powell threw into the pronouncement the need for data dependency. So, we think we are where we were previously – the Fed will move on data received – but the direction of the next move, that is a question. So, let’s look at some data.

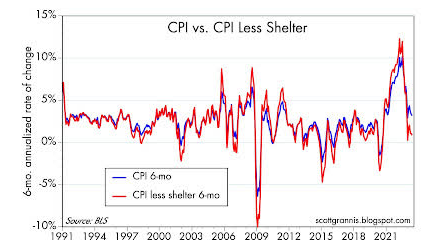

Year over year the Consumer Price Index (CPI) has fallen to 4% after peaking at about 9%. In Chart 1 below, the 6-month annualized change in the CPI is compared to the 6-month annualized change in the CPI without shelter costs. We have written in the past about the importance of shelter costs in the calculation of the CPI (approximately a 30% weight), about how this is a contrived number not reflecting current market conditions and also how this number lags other statistical readings. Without shelter costs, the CPI would be at 0.8% – well below the Fed’s 2% target. Further, the shelter costs calculation continues to drop, as per Chair Powell at his press conference immediately after the Fed meeting, which will provide a downward influence on the calculation of future CPI.

CHART 1

Source: Seeking Alpha

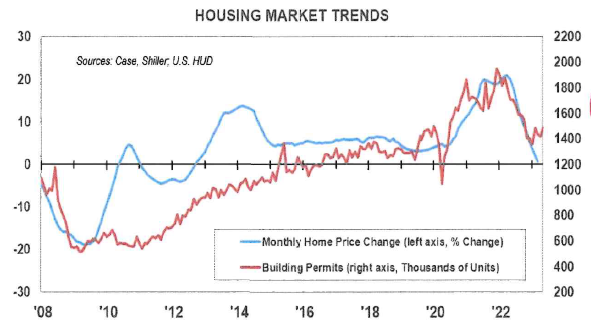

Please examine Chart 2 for more confirmation of the direction of shelter costs.

CHART 2

Source: Seeking Alpha

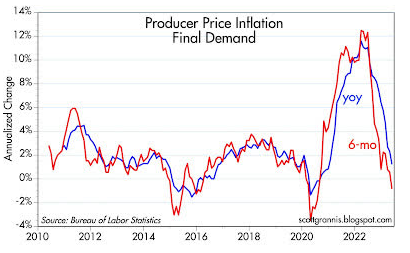

One more slice of evidence about the direction of inflation is found in the following chart which looks at the Producer Price Index (PPI) which is measured one step before the CPI – i.e., prices that vendors are paying. The story is the same.

CHART 3

Source: Seeking Alpha

Following, please find some interesting stats from Bespoke Investment Group, a research house we follow:

1) “App Store” Turns 15. After growing between 27% and 29% annually since 2019, Apple’s App Store now generates $1.1 trillion in billings and sales on a global basis. Fifteen years after its launch in 2008, total sales in the App Store are larger than the annual GDP of all but 16 countries and are larger than the GDP of countries like Saudi Arabia, Turkey, Switzerland, and Taiwan. (Comment: think of the disinflationary effect this one internet application marketplace has had, allowing true price discovery for consumers, and displacing numerous middlemen and expensive brick and mortar stores.)

2) Lower Prices at the Pump. While the price of crude oil was down roughly 40% year over year at the end of May 2023, prices at the pump for U.S. consumers were down 23% over the same period. On the last day of May 2022, the national average was $4.67/gallon compared to $3.57 per gallon at the end of May 2023.

3) Falling CPI, Higher Stock Prices. With headline CPI falling from a peak of 9.1% to 4% year over year, the current period is just the sixth since WWII that CPI dropped more than five percentage points from a 12-month high. One year after each of the five prior periods, the S&P 500 was higher all five times with a median gain of 19.2%.

Source: Bespoke

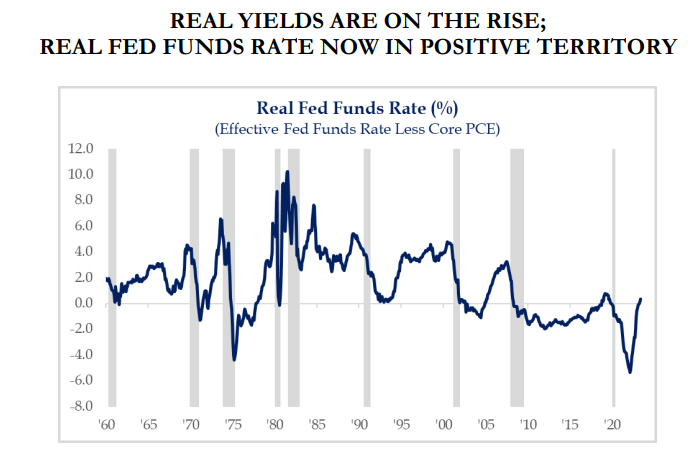

Clearly, inflation is down significantly, and interest rates are up sharply – but is monetary policy restrictive enough so that real interest rates (Fed funds rate less inflation) are positive? Because it is only when interest rates are positive that investors will be motivated to hold cash in a money market fund. Otherwise, they would be induced to spend their cash and this expenditure speeds up the economy, which the Fed is trying to slow to get inflation under control.

CHART 4

Source: Strategas

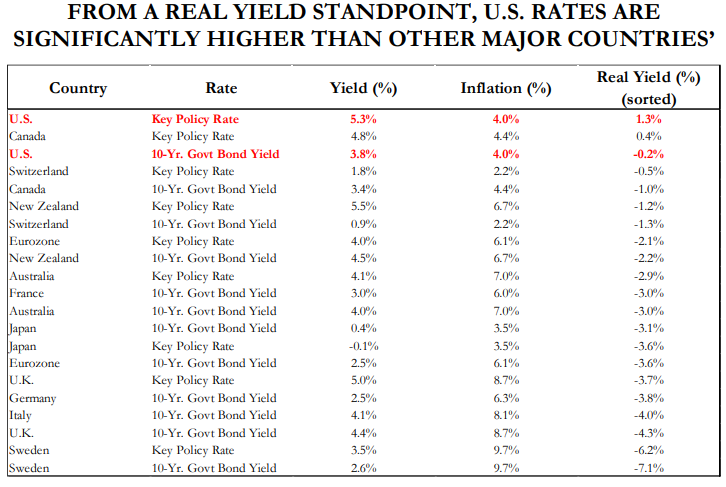

As can be seen above, real interest rates have just turned positive, and they will become more positive as inflation continues its downward slope – without the help of any more interest rate increases. In fact, U.S. interest rates are more “real” than elsewhere in the world as can be seen in the following Table 1.

TABLE 1

Source: Strategas

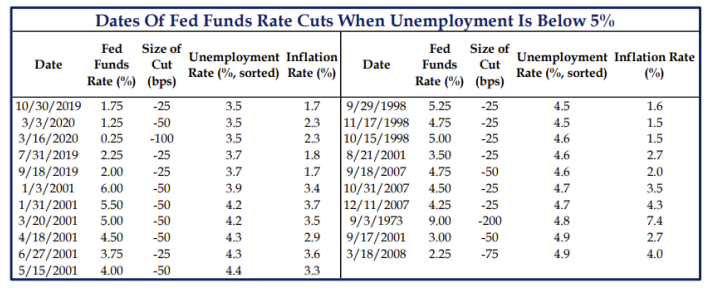

Some analysts have wondered if the Fed would cut interest rates with the unemployment level so low (i.e., 3.7%) to stir the economy?

CHART 5

Source: Strategas

As can be seen by the chart above, it has been done numerous times.

So where are we going with all of this? We think, as we have thought for some time, that the Fed has done its job of cutting inflation, well demonstrated by the charts above. More inflation is yet to come out of the system when lagging price statistics (i.e., shelter) get included in upcoming statistical runs. This should allow the Fed some space to cease making further significant interest rate increases. There might be one more hike of 25bps – we believe for “show purposes”. Chairman Powell, ever since he wrongly used (at least in the eyes of the markets) the word “transitory” to describe inflation last year has had to redouble his efforts to demonstrate to the financial markets his anti-inflation bona fides – to prove he is a Tough Guy. After swiftly raising rates and startling the world with the hiking slope, we believe that the Fed has regained credibility. So, with positive real rates now and with ever increasing real rates coming due to the continued fall in inflation, we think that the present pause in rate hiking may well be extended. If some confusing economic data come into the markets, perhaps Chair Powell will have to make one more small “Tough Guy” hike (25 BPS) to maintain his hard-won credibility. There is also the real possibility that if some clearly good inflation news comes upon the scene, then interest rates can be held – if not lowered, which should be heartening to markets.

UNEMPLOYED YOUNG MANDARINS………

“I went to school to help China rise, not to become some delivery guy.”

“My parents spent their lives working in factories and saving money to give me this scholar’s robe. How can I take it off?”

“Why don’t we all stop going to school, go turn screws in factories, and save ourselves 15 years of effort?”

Source: Economist Magazine

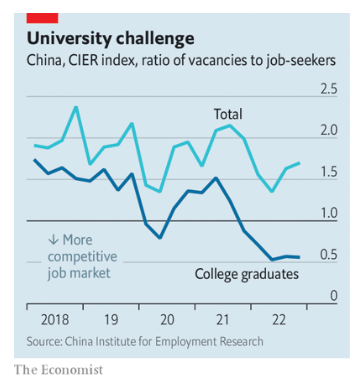

There is some social conflict in China. The youth unemployment rate (ages 16 – 24 years) approximates 20% as of April 2023. It is not that there are not jobs available as can be seen in the following chart – it is that there are not enough appealing jobs for those who have gone to university.

CHART 6

For at least a couple of generations, the Chinese government encouraged study through college and even graduate levels. Competition to get into university was stiff and students studied long hours and parents spent large sums of money for extra tutorials so that their children would achieve more than a laborer’s wage to allow them a better life. But as the economy has slowed, those opportunities have dwindled. Covid did its part to impair the Chinese economy – but so did the government. Crackdowns on technology companies (think Alibaba, Baidu, etc.), real estate companies (think Evergrande, Sunac, Country Garden) and education/training companies (think Tal, New Oriental) – once the “happy hunting ground” for college graduates – have left these corporate giants as “downsizers” rather than employers. An increasing proportion of the jobs available to these overqualified applicants are more menial, safe state jobs with little career future. Exasperation has been voiced by these unemployed Mandarins (“out of school means out of work”) and the government has become a bit defensive. The Chinese Communist Party (CCP) has taken up extolling the virtues of university graduates who choose to work on farms or on assembly lines rather than offices, “to roll up their pants and enter the fields”.[1] This social tension between China’s youth and the government is one of China’s biggest problems. If this is not solved rather soon, then the government will lose legitimacy and from this might spring political disaffection. The Chinese government knows it must rev up its economy in order to provide appropriate employment opportunities for its graduates in order to maintain social and political order.

ENTER THE RAJ………

From downsizing to hiring, from slowing to growing, from old to young – these are some of the distinctive characteristics contrasting China and India. India already is the most populated country in the world having recently surpassed China. It is the largest democracy in the world. Its economy is the fastest growing of the large economies and its economy now ranks 5th in the world in terms of GDP. The Indian diaspora is large and very influential with Indians at the head of some of America’s largest companies (think Microsoft, Google, IBM, etc.). China’s authoritarian government under President Xi did not handle the Covid pandemic very well – disrupting important supply chains for European and American manufacturers, despite having been selected over the past couple of decades as the manufacturing center of choice. Strict Chinese regulations prevented smooth logistical operations. Consequently, international companies have learned a very hard lesson about too much concentration of supply and have begun to diversify supply sources. India is becoming a fast-growing source. Already, Apple is expanding the manufacturing of some of its most important products (iPad, iPhone) to India. European car builders are doing the same, as will others. This is not to say that companies are abandoning China. They are not as of the moment. The Chinese market is too big to ignore. But the logistics concentration risk is also too great. Having second and third sources for supply is prudent and importantly, India also has a very large domestic market for products like mobile phones, cars, etc. as its economy continues to grow and its population continues to get wealthier. India will not eclipse China as a manufacturing center in the near term – but its rate of growth as a manufacturing center will and this should bode well for the Indian stock market.

____________________________

[1] Source: The Economist, https://www.economist.com/china/2023/04/20/what-chinas-graduates-really-think-about-their-job-prospects

A FINAL THOUGHT

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed.

The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results.

We recommend that you compare our statement with the statement that you receive from your custodian.

A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part II & Privacy Policy is available upon request or at www.baldwinmgt.com/disclosures.