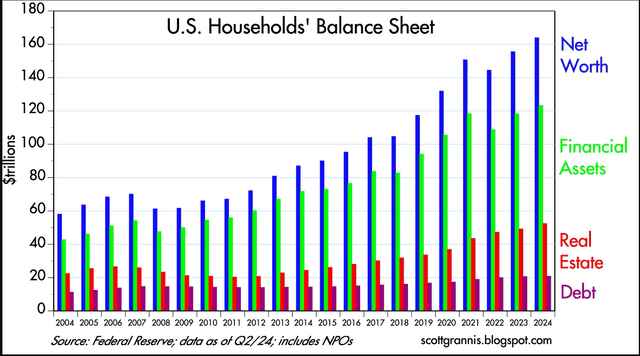

Corporate sales were up, better than expected by Wall Street. Earnings rose, again better than forecasted. Cash flow exceeded analysts’ expectations. Dividends were raised higher than anticipated. Employment levels remained strong. Inflation reduction nearly achieved the Federal Reserve’s inflation target of 2%. Interest rate cutting began in earnest – with lower rates anticipated in 2025. No economic “hard landing” was experienced. No recession occurred and no recession is expected in 2025. This was 2024 economically speaking, which resulted in higher than forecasted stock market prices, and bond markets that generated more than just “coupon” performance. Following is a chart looking at the balance sheet of U.S. households and non-profit organizations:

Chart 1

As can be seen, the private sector has relatively little debt – both as compared to net worth and to total assets. The biggest gains have come from financial assets (stocks, bonds and savings accounts), +149% over the last 20 years. Real estate assets have appreciated some 144% during the same period. Liabilities, meanwhile, have increased only 44%. In short, the private sector is in “rude” health.

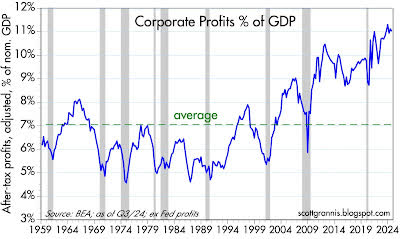

What has driven the appreciation of financial assets over time? We would argue that the prime mover of equity appreciation over the last twenty years has been corporate earnings and margins.

Chart 2

Above, the reader will note how company profits as a % of GDP (Gross Domestic Product, a measurement of an economy’s output) have grown. Further, as American GDP has expanded over time, corporate profits have not only grown along with the economy, they have expanded at a faster rate than only economic growth and taken a larger share of U.S. GDP by expanding margins (i.e., profitability). This increased share of GDP has been rewarded by the markets with much higher stock prices, which has led to a much higher private sector net worth.

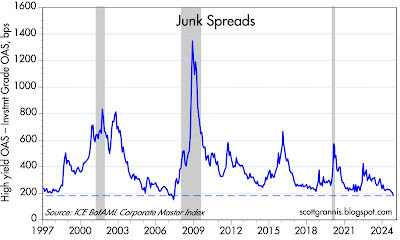

From another perspective – the bond market – let us take another look below at the health of the U.S. economy:

Chart 3

Above, we are examining the spread in yield between high yield (so-called junk) bonds and investment grade corporate bonds. If the spread is wide, as it was in 2008 – 2009 during the Great Recession, then investors are concerned about the health of the economy and in particular, the health of the bond issuer. Investors who demand wide coupon spreads over investment grade bonds believe default risk is high. If spreads are narrow, then investors are relaxed about default risk and are satisfied with a small spread between junk and investment grade securities. As can be seen in Chart 3, the spread between junk and investment grade issues is historically low. Thus, it is the bond market’s determination that economic fundamentals are positive today, which will support healthy corporate profits going forward.

So corporate America is in fine fettle – having had a banner year in 2024 and that year being reflected in both the stock and bond markets’ success. American households continue to enjoy strong balance sheets and unemployment is low. So resilience in the private sector is apparent.

American exceptionalism is a concept that has been written about for generations as the U.S. became the world’s sole superpower politically, militarily and economically. It has been to America that young people from all over the world have come to live their dreams and make their fortunes. U.S. financial markets have developed into oceans of liquidity which are transparent and buttressed with legal and regulatory systems which allow new ideas to be funded. Culturally, America has grown and still grows entrepreneurs. Risk taking has been admired. Failure has not been a badge of shame. Picking oneself up by the bootstraps has been lauded. This has been the environment which fostered American exceptionalism and led to the U.S. dollar’s assuming the mantle of the world’s reserve currency status from the British in the early part of the 20th century.

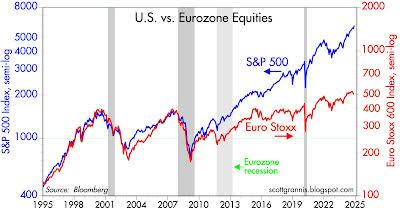

Europeans (including the English) were not eager to cede their top rank position economically, culturally, or militarily to America, but had little choice after the devastation of two World Wars fought on the European continent. Their societies and economies in a shambles, Europeans looked to America for leadership and the U.S. dollar backed by the largest, broadest and deepest financial markets in the world assumed its reserve currency position. After rebuilding, Europe has tried to reassert itself, even going to the length of uniting in a union (the European Union) to compete with America – becoming the United States of Europe. A single currency (the Euro) was developed and greater economic coordination through the European Central Bank was forced upon the many disparate economies. Yet despite all the efforts, the experiment of the European Union has not worked as well as hoped. The Euro has not superseded the dollar, and the Eurozone stock markets have underperformed the S&P 500 for quite some time:

Chart 4

China is the world’s number two economy and has grown mightily since its inclusion in the World Trade Organization (WTO) in 2001. Following the capitalist road, but with a Chinese character, China has become the “workshop” for the world. Cheap labor and plentiful land allowed manufacturers from around the globe to set up manufacturing capacity to feed multinational consumer markets, including the large Chinese market. The early jobs also allowed an impoverished, largely agrarian people to prosper, creating some wealth and a middle class.

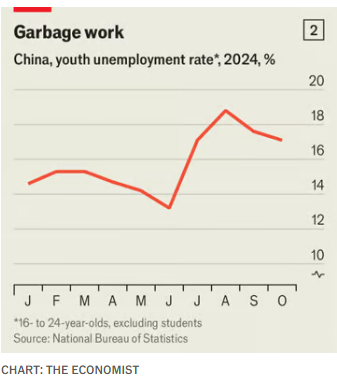

This newfound wealth, in turn, fostered more and a higher order form of wealth creation based on industrialization and technology. Many Chinese left their country to get educated in the west and then returned home, bringing back their new knowledge. The phenomenal expansion of the Chinese economy within a timeframe of a couple of generations has created a worthy competitor for America. But we would argue, China is not yet ready to replace U.S. leadership of the world. Militarily, the Chinese have assembled an impressive military if one simply looks at numbers of personnel, ships, airplanes, etc. The quality of those forces is untested, however, as the last time the Chinese were in a real fight was the Korean War – whereas the U.S. forces have been fighting battles all over the world since World War II. Politically, the Chinese under the current regime have earned a reputation for being brutish. There are continuous skirmishes with neighbors in the South China Sea. There are border fights with India in the Himalayas. There are island shoving matches with the Japanese. Economically, the Chinese economy has stalled since Covid. Animal spirits are gone. Young people, where the unemployment rate approximates 17%, are “lying flat” – a Chinese phrase for just going through the motions of working:

Chart 5

Young people are dispirited because they emerge from college with high expectations of getting a good job and instead are underemployed or unemployed despite years of hard university work and parents who sacrificed to pay for education. The real estate crisis which has plagued China for years is getting little better. There are hundreds of empty buildings or partially finished apartment houses with strapped developers who do not have the funds to finish projects already sold to people. And those who have purchased have no way of recovering their money because the developer is bankrupt. This all occurred because President Xi decided to reform the building industry and enacted regulations which crippled builders. The house of cards has collapsed – but the government has refused to acknowledge the disaster. Every couple of weeks a new government support policy is announced which applies another band-aid to the gaping wound. The situation will not improve until reality is acknowledged. So, again we would argue that China is not yet ready to take on the leadership role to which it aspires. This has been reflected in the markets as shown below:

Chart 6

We continue to believe that the U.S. is currently the preeminent economy in the world with a market system which is deeper, broader and more liquid than any other, supported by a legal and regulatory system which provides transparency and protection for investors, and a culture which champions risk taking. To date, there is no other economy which can or does compete. But the U.S. federal debt balance is a real threat to American exceptionalism and to the position of the U.S. dollar as the world’s reserve currency. Investors’ concerns are rising about American profligacy. If investors no longer feel safe holding U.S. assets like the dollar, then America will be treated like any other borrower and will be forced to change its spending habits – not necessarily on America’s time schedule, but on the market’s, which could be much harsher.

So for the New Year, let us look at what we think is important for our rationale:

- Corporate earnings are expected to increase some 12% – 14% in 2025;

- Dividends are presumed to increase apace;

- Company management teams will work to maintain/improve profit margins;

- Greater investment in and use of AI (Artificial Intelligence);

- Interest rates are slated to decline perhaps another 50 basis points;

- Unemployment should range from 4%-5%;

- A more accommodative regulatory environment is expected for U.S. businesses;

- Previous tax cuts will be maintained with some new introduced;

- Tariff use may rise;

- Deficits and government debt will become a focus of investor attention.

Through the third quarter of 2024, companies have largely surprised Wall Street to the upside. Sales, earnings, cash flow and dividends declared have exceeded expectations with generally optimistic forward-looking statements about upcoming quarters and projections for 2025. In short, business has been good and looks to remain good in the coming year. The most enthusiastic managers hail from technology – more specifically those working with Artificial Intelligence. AI is the shiny new object in our modern world and those intimately involved (think Nvidia, Microsoft, Amazon, Alphabet, etc.) have been dubbed the “Magnificent Seven.” These seven stocks have led the stock market’s advance over the past year and sell at valuations that many consider extraordinary, if not overvalued. But these stocks have rocketed to their lofty prices because they have dramatically exceeded expectations for sales, earnings and cash flow – and they have done so quarter after quarter. The market seems to be comfortable that these companies have earned their valuations. Further, the management teams at these “Magnificent Seven” continue to forecast bright and maybe even brighter days ahead. We are in the early days of a technological tectonic shift – but more on that later. The other 493 companies in the S&P 500 are selling at much more reasonable values, so we think that there are ample investment opportunities in many companies outside of the “Mag 7”. These are the companies which will take advantage of AI, use it in their business and become more efficient while driving new sales to enhance margins and increase profitability. This will be the next stage of AI.

Interest rates fell during 2024 and are expected to continue in 2025. The course may not be straight or steep. Monetary policy is still restrictive, not neutral, and there has emerged a noticeable weakness in employment. While a 4.2% unemployment rate is close to full employment for the U.S., the Fed’s dual mandate of managing inflation and employment rates has turned its focus to the labor question, as the Fed has stated that inflation is on course to achieve the Fed’s 2% goal. Interest rates will fall more in 2025 – which should further support equity prices throughout the year.

Business regulation is a burden and an expense with which no business leader wants to deal. Unfortunately, because of too many bad actors in the business world, regulations are a fact of life. The degree of regulation, however, can be titrated – and currently too many in business think that regulations controlling their industry are too burdensome. With Republicans declaring a war on business regulations, animal spirits have been unleashed. The prospect of fewer and less burdensome rules by which to conduct one’s business on the horizon should lower expenses, drive efficiencies and promote margins – all of which will support higher stock prices. Taxes are another expense which at the very least will not rise as once feared and may go down. Again, this is a campaign promise of the Republicans and is music to many a citizen’s ear. All are supportive of a growing economy which in turn should support stock prices.

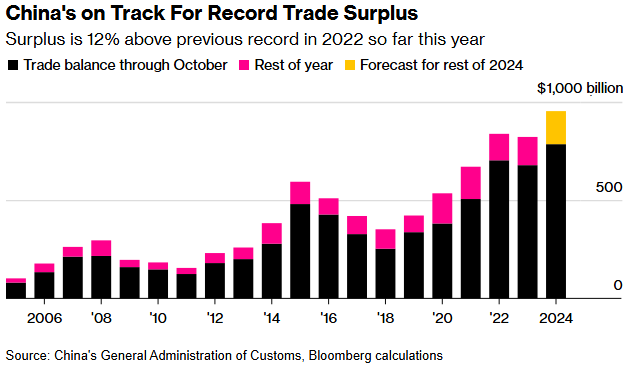

But we do not believe that increased use and broadening of tariffs, potentially starting/inflaming trade wars, is helpful for American economic growth or international relations. Certainly, the last time trade tariffs were instituted against the Chinese, American consumers paid more for Chinese manufactured goods and the Chinese retaliated by slapping tariffs on American farm products, which devastated U.S. farmer incomes. American farmers in turn were supported by direct federal government transfers. So the tariffs paid by some American consumers went to pay the transfers for American farmers. At the end of the day, some American consumers paid higher prices for goods and American farmers lost access to a big market in China, losing sales to Brazil. Further, as per the chart below, clearly trade tariffs instituted against China years ago and enlarged in subsequent years have had no beneficial effect on the U.S. trade deficit with China:

Chart 7

Another way to solve the U.S. trade deficit problem with China in particular (i.e., the point of tariffs) would be to depreciate the dollar. This would certainly restrict imports as they became too expensive, and promote American exports, as they became cheaper with a lower dollar. But in cheapening the dollar to solve the trade deficit problem, one damages the dollar as the world’s reserve currency. Who would want to trade and hold investments in a depreciating asset – i.e., the U.S. dollar? The trade deficit is the mirror image of the American capital account, where foreign nations have for generations purchased U.S. stocks and bonds with their surpluses. Reducing the U.S. trade deficit will in turn reduce the U.S. capital account. Lowering the value of the dollar would import some international inflation and potentially lower the American standard of living. We are not sure that this is the direction we should go as Americans. We do not have an answer – but we are sure instituting and expanding a broad swathe of tariffs to cure our trade deficit problems with the Chinese, the Europeans, the Japanese, etc., is not a satisfactory answer and we do not think the markets will think so either.

We have worried aloud before about our nation’s debt level and its threat to America’s leadership position, as well as its threat to the dollar being regarded as the world’s reserve currency. Earlier in this Commentary we have outlined why we do not think in the near term that there is still any credible competitor to the United States’ leadership or to the dollar’s supremacy. However, the conversation about America’s debt levels is getting louder and more frequent. More people are concerned enough that a Department of Government Efficiency (DOGE) has been created under the joint leadership of Elon Musk and Vivek Ramaswamy. Since this “department” has no authority, it can only influence – not execute. So we shall have to see how effective the effort will be. The goal of deficit spending reduction, which will lead to debt reduction, is laudable. Success would be cheered by the markets.

We mentioned earlier that we thought we were at the start of a technological tectonic shift with the discovery of AI. Some very smart people are spending billions of dollars to keep up with competitors. The market has determined that this technology is real and will be meaningful to humankind for generations to come. No doubt there might be a bit too much ebullience in some quarters about AI. No doubt there will be corrections in market valuations from time to time as the future does not progress as smoothly or as quickly as some envisaged. But we believe that only the inventors’ first steps have been taken and now it will be the users who will start to experiment with AI to transform their businesses.

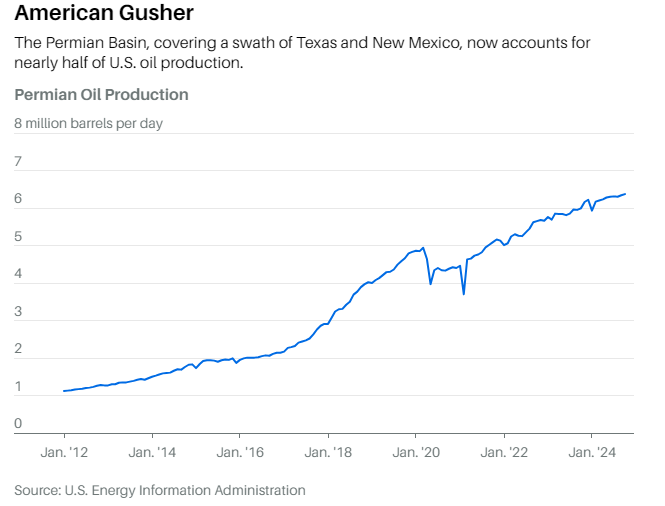

For example, in the “oil patch”, Americans have a long history of innovation. The preeminent basin in the United States is called the Permian, located in West Texas and eastern New Mexico. The Permian has been drilled for generations and has yielded billions of barrels of crude oil and natural gas. Today, the Permian Basin accounts for nearly 50% of American production of 13 million barrels/day:

Chart 8

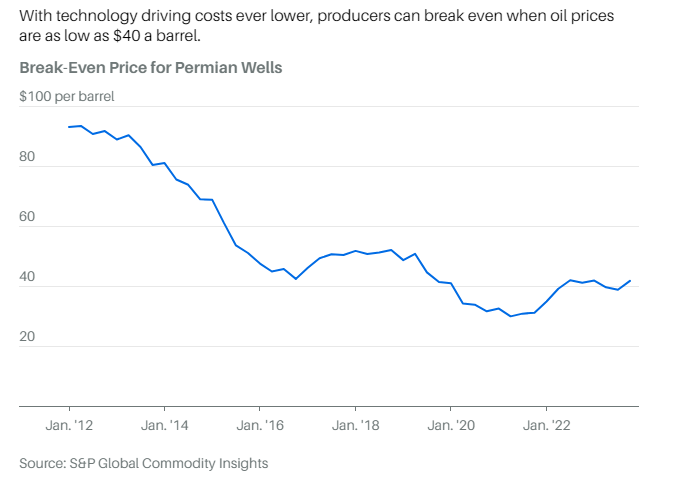

AI has come to the Permian. The Basin was formed over millennia in layers. Those layers are being drilled horizontally, and the well bores are being perforated at certain intervals according to determinations made by AI. The objective is to recover more hydrocarbons from each well bore, thereby increasing production and lowering cost. Technology has driven the breakeven cost for Permian wells down to $40/barrel from over $90/barrel back in 2012:

Chart 9

Offshore, oil companies use seismic imaging to locate potential drill sites thousands of feet below the waterline. Evaluating the images used to be time consuming. According to the head of SLB’s (a major oil field service company) digital business, the time to evaluate seismic images has been compressed from 18 months to 18 days. This is an amazing order of magnitude enhancement in speed to final investment decision (FID) which will positively impact oil company drilling efficiency and profit margins dramatically. The aforementioned is just one example of what is possible, if not probable.

Overseas, we would attach one word to most markets as a descriptor – cheap. In China, the markets are trading some two standard deviations inexpensive to the American market and to their own history. The fundamental reason for such a depressed valuation, we believe, is central government mismanagement. There are some great companies in China led by skilled managers. Unfortunately, the economic and political environments are not ones that inspire investor confidence. Too much political power has been ceded to President Xi and he has become too meddlesome in economic affairs, instead of allowing market mechanisms to sort out the economic problems which have arisen. The Chinese markets are inexpensive – but also according to too many investors, uninvestable. We are hopeful that one day in the not-too-distant future investors will get back to making money in Shanghai and Hong Kong. But picking fights with neighbors, dumping products on international markets and not attending to fundamental problems at home would suggest that becoming investable again is some time in the future. In Europe, again there are talented management teams who lead world class companies in their industries. European markets should not be shunned and they are cheap, also. But they have been inexpensive for years. Europe, writ large, may be a “value trap.” Yet we like to own specific companies trading on various exchanges because they are an integral part of an important supply chain supporting important producers of necessary products. Eurozone politics are becoming a bit frayed, and these politics are spilling over into international economic decision making. There is also a war still going on in Eastern Europe. So we would not be buyers of any country ETF – but would like to own individual names or managed funds. India (like Vietnam, Malaysia, Türkiye and Indonesia) is trying to supplant China as the world’s workshop. We think they all will have a role – but only India comes closest to becoming a complete replacement for China. It has an increasingly educated and growing population. Moreover, India has a business-friendly government and a number of world class companies successfully competing in America and Europe. The Indian economy is the fastest growing large economy in the world. Militarily, the Indians are coming closer to the U.S. and are now part of an alliance along with the U.S. and Australia to “fence in” China. The Indians and the Chinese are more than competitors, with a long history of border battles in the Himalayas. India aspires to replace China in world trade. It is not there yet – but it could be so in the future if both countries remain on their current growth trajectories. Japan is waking after a decades long commercial sleep. The economy still has not completely broken free of its fight with disinflation. But there are encouraging signs. Corporate governance is being reformed so that shareholders are better recognized as owners of the business and not simply being ignored. Merger and acquisition activity is stirring. Politics are unsettled at the moment. Chinese assertiveness has put the Japanese on alert and brought them closer to the U.S. Japan’s central bank is raising interest rates while the rest of the world is lowering rates. Japan is an improving situation and not the “basket case” it had been for years due to its fight with disinflation.

This past year was better than expected – certainly in U.S. markets. Companies surprised analysts to the upside and their stocks reflected those pleasant surprises. Inflation cooled its rise, and the Fed responded by cutting interest rates. Other central banks around the world, except for Japan, also cut their interest rates, and other equity markets responded. So 2024 is ending on a high note. In 2025, we expect U.S. corporate earnings to continue to increase with rising company sales, cash flows and dividends. Interest rates should decline, lending further support to stock and bond prices. Unemployment should remain within a range approximating where it is and thus historically healthy. Additional support for investor animal spirits will be a reduction in regulation and no increase in taxes, if not a reduction in taxes. Enhanced government efficiency as promised by DOGE will also boost investor psychology if successful – demonstrating that a heretofore considered impossible task was made possible. A counterbalance to all the above would be the execution of a broad suite of tariffs. Four hundred and ninety-three members (i.e., ex the “Magnificent Seven”) of the S&P 500 are not outrageously priced and there are values to be found in this collection of names -especially as the use of AI spreads. Europe is inexpensive, with world class competitors to U.S. companies to be found in the Eurozone. Asia, ex–China, has interesting opportunities as does Japan. China is cheap – but probably a value trap.

HAVE A VERY HAPPY HOLIDAY SEASON!!!!!

A FINAL THOUGHT….

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed. The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results. We recommend that you compare our statement with the statement that you receive from your custodian. A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part 2A & Privacy Policy is available upon request or at www.baldwinmgt.com/disclosures.

Peter H. Havens, Chairman

Peter Havens founded Baldwin Investment Management, LLC in 1999 after serving as a member of the Board of Directors and Executive Vice President of The Bryn Mawr Trust Company. Previously he organized and operated the family office of Kewanee Enterprises. Peter received his B. A. from Harvard College and his M. B. A. from Columbia Business School. He serves as Chairman of the Lankenau Institute for Medical Research. He is a Board member of AAA Club Alliance, Main Line Health, The Lankenau Medical Center Foundation, and the former Vice Chairman of Main Line Health. He is a Trustee Emeritus at Ursinus College, Chairman Emeritus of the Board for the Independence Seaport Museum, former Trustee of the Leukemia Society of America, and a former board member of Main Line Health Realty and Lankenau Development Inc. He was also the Chairman of the Board of Petroferm, Inc. and a Board member of Nobel Learning Communities Inc.