Underfoot there has been something of a shift in investment strategies. So far, it is not huge in scope or long in duration – but it has been noticeable. Growth stock investing (typically focused on companies with high revenue growth, perhaps earnings growth and higher price/earnings or P/E ratios-think Facebook, Amazon, etc.) which has been the “rage” for better than a decade has taken a backseat to value investing (companies with slower earnings and revenue growth, but priced with low P/E ratios – think General Motors and Citigroup) in the first quarter of 2021. Why?

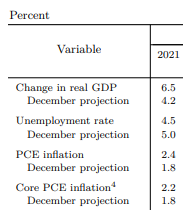

In short, we believe it is because investors believe in a worldwide economic recovery, post the Covid-19 pandemic. As shots are getting into arms, prognosticators are getting more ebullient about recovery prospects. For example, at the March Federal Reserve Board meeting, the Fed dramatically increased its outlook for 2021 US economic growth as well as lowering its projected unemployment rate for year-end:

CHART 1

Similarly, the economic outlooks for China, Japan and India are brightening. In Europe, 2021 began a bit brighter, but has become more muddled as the Eurozone is under another “lockdown” due to a resurgence of Covid-19 because of vaccine distribution difficulties. Where vaccines are being successfully and efficiently administered, hopes are rising that economies will open.

Economic growth is great for companies’ bottom lines. But analysts, leaning on prior experience, extrapolate that along with faster economic growth and higher corporate earnings will necessarily come higher inflation and interest rates. Increasing interest rates create a higher hurdle for the valuation of equities. The higher the interest rate, the lower the P/E ratio that a market will award any given stock because of competition from a liquid alternative, bonds. So, rising interest rates are generally considered a “headwind” for stock prices – especially for growth stocks which sell at lofty P/E ratios. Value stocks, which usually sell at lower P/E ratios, are somewhat shielded because they are cheaper and are generating earnings today, not in some far future period. Helping the general investment case for stocks in this supposed rising interest rate environment are increasing earnings in a growing economy. So, it is a bit of a race in the marketplace as to which factor is going up more quickly – interest rates or earnings – and thus how should a stock market react. If earnings go up more quickly than interest rates, then the market is getting cheaper over time and equities have “headroom” to appreciate. If rates move up more rapidly than earnings, then the market is getting more expensive and stocks probably will depreciate in value.

Beyond the “blanket” consideration of rising interest rates being bad for stock prices, there is also a nuance when distinguishing between growth and value strategies. This is especially true coming out of an economic recession. Throughout a recession, growth companies (think Netflix and Amazon) may well be shielded economically because their products are demanded no matter what the financial climate. These companies prospered during the pandemic and their stock prices reflected as much, thus the higher P/E ratios. Now with the pandemic hopefully “in the rearview mirror”, more economically sensitive companies (think value names like Exxon and JP Morgan) may “snap back” and register comparative earnings which may well outshine their growth colleagues. This would represent a “reversion to the mean”.

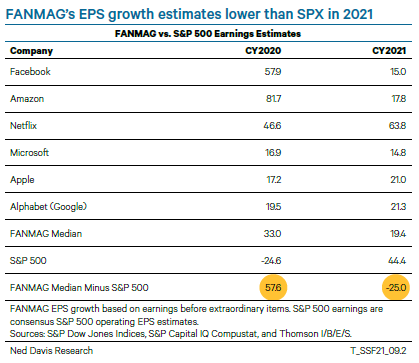

CHART 2

In Chart 2 above, the reader will see a list of the growth stocks most associated with and responsible for the outperformance of growth stock investing for the past several years. In the column labeled CY (Calendar Year) 2020 the median earnings growth for those companies is listed as 33.0% vs. the median S&P 500 earnings growth of -24.6%. In the column for 2021, the median earnings growth for those selected companies slows to a still handsome 19.4% but the median mark for the S&P 500 is 44.4%. This is a substantial “snapback” and reversion to the mean. This change of fortune also likely has contributed to a shift of investor dollars out of a growth strategy and into value.

So it is interest rates – their direction (going up or down) and level (low as today or high as they were in 1980) – which will largely determine the valuation of any stock market or bond market and certainly influence the success of a particular investment strategy (growth or value). Ameliorating or augmenting the interest rate effect will be earnings growth or decline.

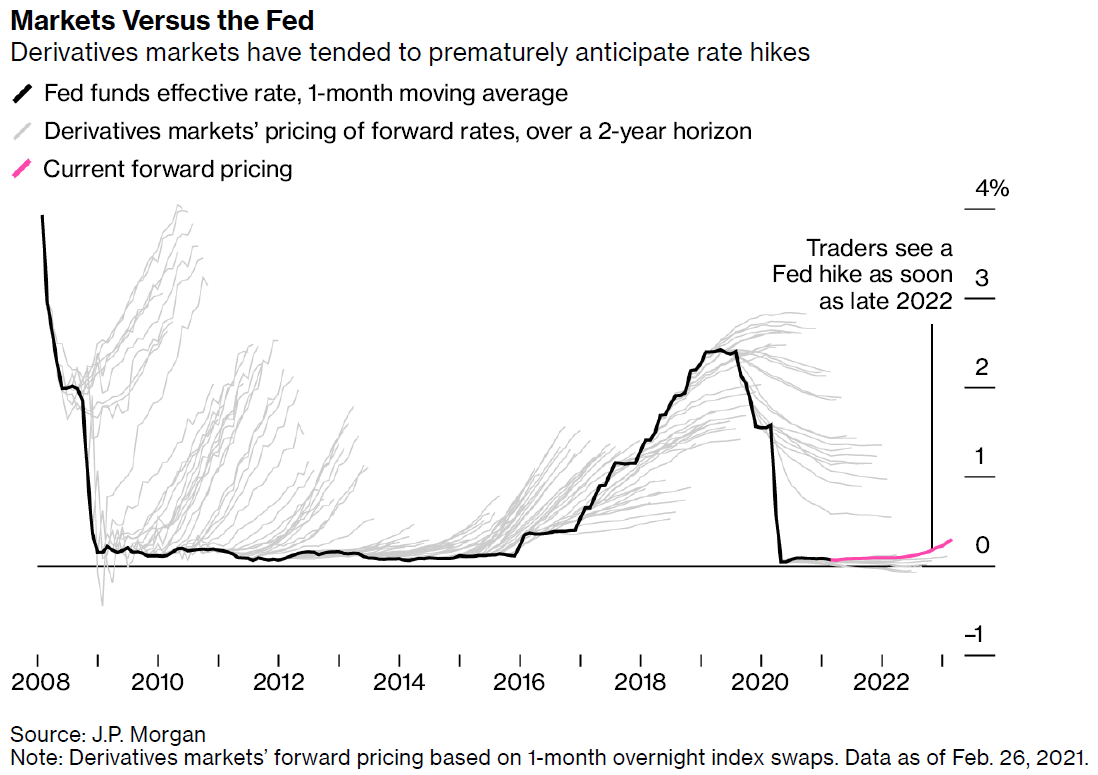

What is the situation today? Economically, the U.S. is on a decided uptrend – not only because it looks like the country is coming out of the pandemic, allowing businesses to reopen, but also because of extraordinary fiscal support (the $1.9T American Rescue Act just passed) and monetary help (near 0% interest rates and huge monthly bond buying by the Fed). With all the aforementioned assistance, bond market investors are projecting rising inflation in the near future, selling bonds and increasing market interest rates. Oppositely, the Fed continues to pledge that rates will stay low through at least 2023 and that it will continue to buy a significant volume of bonds on a monthly basis. So, there is a “standoff”. We believe the Fed. We have seen bond market tantrums in the past and it has never been a good strategy to bet against the Fed. In Chart 3 below, please note how many times, as depicted by gray lines, since the Great Recession that bond traders incorrectly anticipated an increase in interest rates by the Fed – only to be disappointed and have rates go back down.

CHART 3

Interest rates may stay a bit above the floor recently set in late 2020 as economic recovery becomes more obvious. But we do not think interest rates will increase enough to snuff out the U.S. recovery – because the Fed will not allow that to occur. Corporate earnings should have a very nice bounce in 2021, especially in industries that were damaged in 2020 (think hospitality, restaurants, airlines). The rate of earnings increase in these businesses will probably shock on the upside – a reversion to the mean and a return to growth. The “growth darlings” may not be so impressive with their comparative earnings growth reports, because they did not suffer so much in 2020. Nevertheless, growth company profits should be handsome and would be most welcome in any other year. We think that there will be some rotation out of growth stocks, trimming winners, and into more value-recognized names. However, we are not yet convinced that there will be a wholesale conversion from a growth to value strategy because investors still appreciate growth and consistency – two hallmarks of the growth stock strategy.

Sumo Wrestling…

In Japan there is an ancient form of wrestling still popular today in modern Japan. After a prolonged ritualistic ceremony of prayer, two giant Japanese wrestlers lunge at one another from opposite sides of a circle, intending to push one or the other out of the circle to win the match. During the match there is a great collision of flesh with arms flailing to defeat the opponent.

This, it seems to us, is the state of the U.S. relationship with China. America and China represent the two biggest economies in the world today. The U.S. is the economic leader with China “fast on its heels”. America is the military leader of the world and has been the international “policeman” for decades. China is spending lots of money on defense and is becoming a formidable power. The U.S. sees itself as the political leader – but China has recently under President Xi exercised a more muscular political philosophy domestically and internationally and is no longer willing to concede easily that it “plays second fiddle” to the U.S. in this sphere. China and America are competitors. We also have a symbiotic relationship because both countries buy substantial goods and services from one another. Thus, we need one another, and the world certainly does not need the two biggest economies to be at odds with one another. It would be bad for business. Healthy competition is good.

According to foreign policy experts, the relationship between China and the U.S. is evolving into a new dynamic. Pictured as the “rising” power, China is more confident economically, militarily and politically. As a nation it seems more willing than in the past to take risks in Hong Kong, Taiwan, on the Indian border and around the South China Sea. China also seems more willing to upset the “old rules” and the global status quo that has been policed by America. The U.S., on the other hand, is reluctant to cede influence (either soft or hard) and is trying to maintain its position. The Chinese bridle at this, saying that the U.S. is trying to “keep China down”.

We think that this new stage of the American/Chinese relationship must be watched closely. There is no reason why it must devolve into something ugly – a new Cold War. But that possibility cannot be ruled out. If there were to be a rupture, there would be significant economic consequences for the world and markets would react badly. We do not think that this will be the path chosen. But we need to watch this situation.

PREDICTIONS FOR 2021

- Inflation will stay low. Yes – So far, so good.

- Interest rates will remain low. Yes – A bit of a “backup” but still low

- The dollar will weaken. Yes/No – Dollar has been weaker, but with slight “backup” in interest rates, the dollar has regained some strength.

- Oil will stay in a pricing range of $50-$60/bbl. Yes – there was a rally, but that has lost some “steam.”

- World GNP (Gross National Product) will rebound strongly. Yes – Getting stronger with fiscal stimulus & monetary support.

- Corporate earnings will rebound strongly. Yes.

- Investor “risk appetites” will increase. Yes – Still believe.

- International equities will outperform U.S. equities. Yes/No – International stocks rallied early, but have given up some advantage.

- In the U.S. infrastructure spending will jump. Yes – The Biden administration is submitting a big plan.

- U.S. stocks will have a good year with some rotation out of “tech darlings” into more economically sensitive names. Yes – see above.

A FINAL THOUGHT

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed.

The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results.

We recommend that you compare our statement with the statement that you receive from your custodian.

A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part II & Privacy Policy is available upon request or at www.baldwinmanagement.com/disclosures.