As this is being written U.S. markets are being buffeted by tariff threats and reciprocal tariff threats, challenges to sovereignty in Canada and Greenland, and talk of using military force to deal with the drug cartels in Mexico. The war between Russia and Ukraine grinds on with some seemingly odd twists among supposed allies, and a Middle East truce which now appears to be on life support. Suffice to say that the crosscurrents affecting markets today are head spinning for too many investors. While we may be in the midst of a market correction – which is normal and healthy following the prolonged market advance investors have enjoyed for the past couple of years – it is uncomfortable.

Recently, 98% of fourth quarter earnings results for S&P 500 companies have been reported: U.S. companies had a very good final three months of 2024, especially as compared to Wall Street expectations. Sales rose 5.4 %, exceeding predictions of +4%. Company earnings increased 16% year over year, well ahead of +12% expectations. Almost as importantly, management outlooks for Q1 2025 were generally positive, as they were for the entire year. So corporate America ended 2024 well and most looked forward to 2025. Wall Street analysts were also in agreement. The American consumer too had a very good year in 2024. With another substantial gain in 401(k) values thanks to strong stock and bond markets and with real estate values up for another year, the consumer’s balance sheet was again enlarged. State finances also had a good year due to higher tax receipts as exemplified by Texas’s paying down some of its indebtedness. The Federal government, however, did not fare so well – again running a huge deficit, further piling onto its already large debt load.

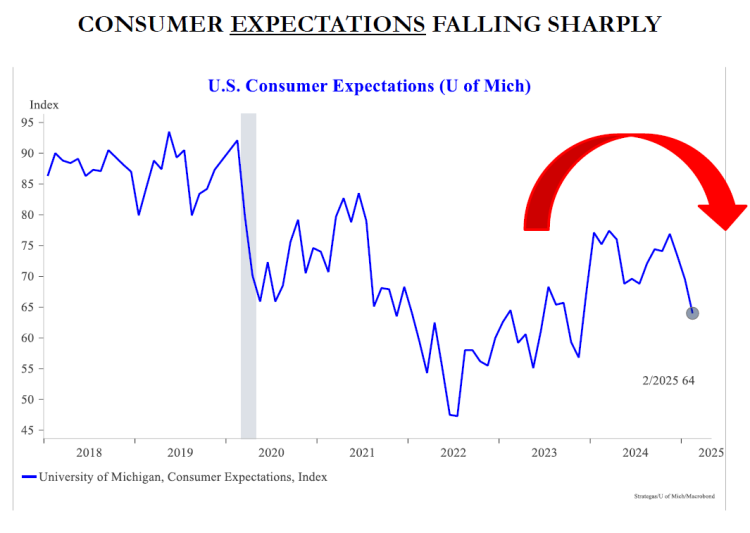

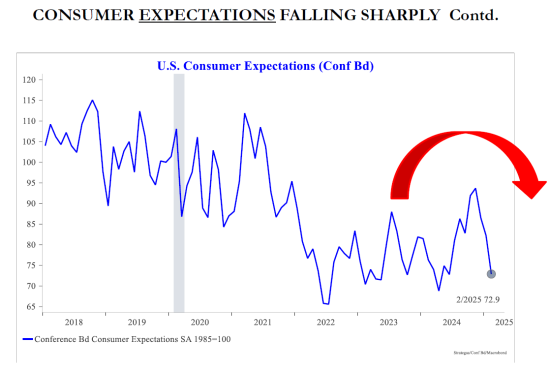

It is this federal debt which is the focus of attention. Efforts to slash government costs have led to the establishment of the Department of Government Efficiency (DOGE), led by Elon Musk, and charged to eliminate waste. Every day there are new reports of mass federal employee firings or department closures. Unfortunately, DOGE has not always executed their charges expertly and the appearance of a lack of empathy and forethought has unnerved quite a few people from across the political spectrum. Besides reducing costs, efforts have been made to cut trade deficits and raise monies through the imposition of new taxes or tariffs. This too has raised concerns as can be seen below in Charts 1 and 2 from two different sources.

CHART 1

CHART 2

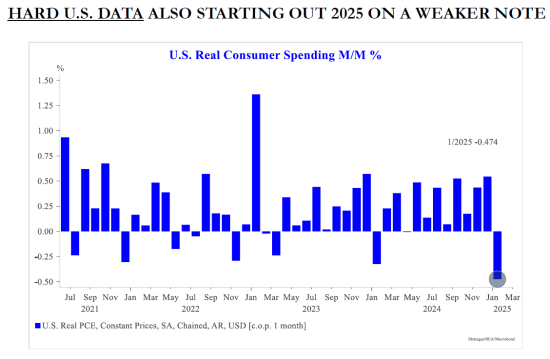

The two charts above measure Consumer Expectations and tell the same story: the U.S. consumer (approximately 70% of the American economy) has become quite nervous in the opening months of 2025. These worries are also reflected in Chart 3 where real consumer spending fell sharply in January 2025.

CHART 3

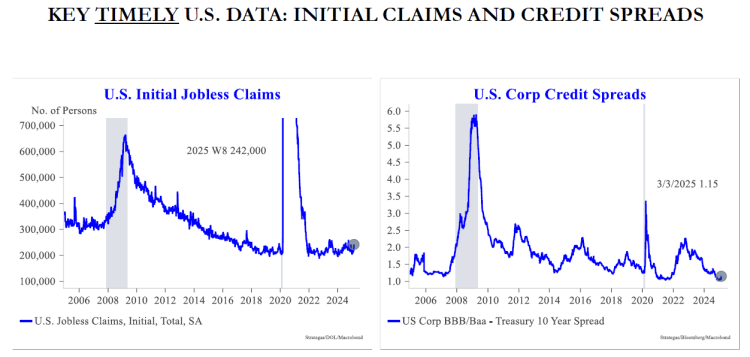

So far, the mass firings have not shown up in the weekly initial jobless claims reports (see Chart 4). We think this is just a matter of timing. And so far, the credit markets have not “blown out” (i.e., yields on “junk” bonds do not demonstrably exceed those of Treasurys, which would signal bond market distress). The bond market still is not predicting a recession.

CHART 4

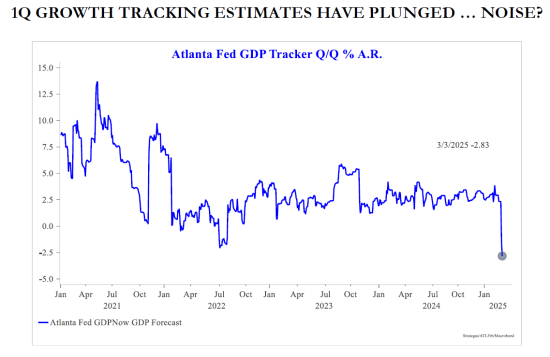

But the Atlanta Fed GDP Tracker is showing a large drop (see Chart 5), which is predicting a sharp economic slowdown in Q1 2025 to negative growth.

CHART 5

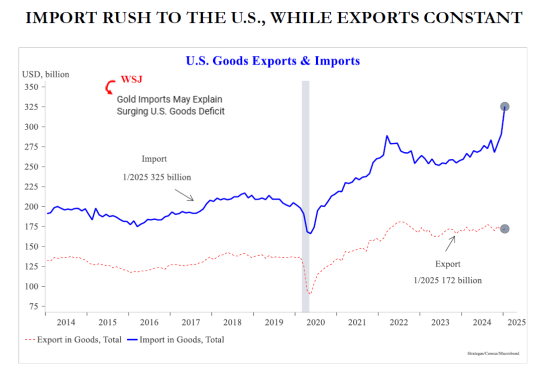

This is worrisome. It is not a definitive signal that a recession will soon be – but it is a troubling sign. (The official definition of a recession is two consecutive quarters of negative GDP growth.) A very good explanation, outlined in Chart 6 below, is that many businesses, in anticipation of import duties (tariffs), decided to pull forward their international goods orders. One can see the sharp rise in imports in early 2025, while exports essentially remained flat. This overwhelming rise in imports created a larger than normal trade deficit, which acted as a significant negative in GDP calculations. So one might consider this anomalous due to political influences, not economic.

CHART 6

Nevertheless, GDP performance for the first quarter of 2025 likely will be much weaker than previous quarters, and the strain on investors trying to separate “the noise” from the true economic results is being demonstrated in almost daily stock market volatility, mostly downward. Business leaders hate uncertainty. Investors hate uncertainty even more and the headlines of 25% tariffs on some Canadian goods and 200% tariffs on European wines is alarming. But will 25% tariffs on certain goods actually raise prices on those goods by 25%? It depends, according to a study done by Moody’s Analytics. Tariffs will raise prices – but perhaps not as much as feared. Following, please find four charts which categorize products as: 1) a commodity with lots of competition, 2) a niche product, 3) a premium product without alternatives, and 4) a higher sticker price product with limited alternatives.

As can be seen, depending upon the product, its market’s competitiveness and the country of origin, a 10% or 20% tariff will not necessarily translate into a 10% or 20% price increase. Again, tariffs are a tax and will raise prices on goods. By how much – that answer is a bit more nuanced.

CHART 7

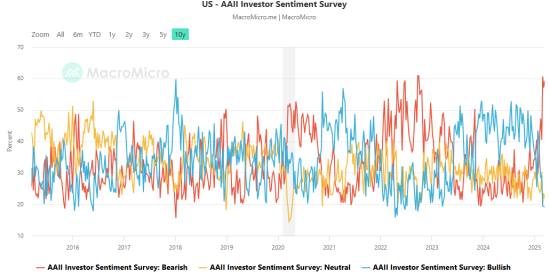

Investors and markets entered 2025 in quite good shape. Analysts were enthusiastic in their outlooks for the new year as were most company managements. Sales and earnings for the upcoming 12 months were slated to show meaningful improvement over results secured in 2024. But haphazard federal employee dismissals, federal department closures and chaotic tariff impositions have damaged consumer and investor sentiment. This damage to investor sentiment is demonstrated in Chart 8 below with the spike of the red line to the far right of the chart.

CHART 8

Openly, pundits are voicing a new concern about recession in the U.S. Further, if a recession were to happen in 2025, it would be a “manufactured” recession – i.e., American economic activity would stagnate due to confusing policies and actions coming out of Washington. We are not ready to project a recession yet – but we are closer than we were just a few short weeks ago. The speed with which change is being forced on the U.S. economy and the manner with which it is being imposed on American business, as well as international partners, has thrown a lot of “sand into the gears”. This sort of disruption is incomprehensible to most – because it has never happened at such speed and scale. As a result, things are not and will not for some time run smoothly. Consequently, forward corporate earnings are at risk. Counter-balancing, at least to some extent, the economic upset are the management teams at the companies in which we have invested. They are paid handsomely to anticipate, and we believe that the management teams we have selected are already hard at work defending corporate strategies and looking for opportunities to grow amidst the chaos. Winners take advantage of disruption. Losers are disrupted.

CRYPTO RESERVE??????

It is thought by some in Washington that it would be a good idea to establish a crypto reserve to back the U.S. dollar. We have written often about our future concerns regarding the value of our American currency if we continue to be profligate in our spending. But we are not in favor of trying to establish a reserve using something with no intrinsic value to back the U.S. dollar. Further, we think it foolish and deleterious to the value of the American dollar to back the world’s reserve currency with something which has no intrinsic value. The U.S. is the global reserve currency issuer by a very large margin. Foreign reserves of the greenback are 54%. The Euro stands number two at 19% and the Japanese yen is at 5%. International trade is largely done in dollars because the American economy is the largest, wealthiest, deepest and most trustworthy economy in the world. People still want to do business with the U.S. and they still like getting paid in dollars, because it is a currency which is readily tradeable around the world. America remains the most innovative and productive economy on the globe. To bolster the American currency, we need only to incentivize economic output.

A FINAL THOUGHT…

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed. The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results. We recommend that you compare our statement with the statement that you receive from your custodian. A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part 2A & Privacy Policy is available upon request or at www.baldwinmgt.com/disclosures.

Peter H. Havens, Chairman

Peter H. Havens, Chairman

Peter Havens founded Baldwin Investment Management, LLC in 1999 after serving as a member of the Board of Directors and Executive Vice President of The Bryn Mawr Trust Company. Previously he organized and operated the family office of Kewanee Enterprises. Peter received his B. A. from Harvard College and his M. B. A. from Columbia Business School. He serves as Chairman of the Lankenau Institute for Medical Research. He is a Board member of AAA Club Alliance, Main Line Health, The Lankenau Medical Center Foundation, and the former Vice Chairman of Main Line Health. He is a Trustee Emeritus at Ursinus College, Chairman Emeritus of the Board for the Independence Seaport Museum, former Trustee of the Leukemia Society of America, and a former board member of Main Line Health Realty and Lankenau Development Inc. He was also the Chairman of the Board of Petroferm, Inc. and a Board member of Nobel Learning Communities Inc.