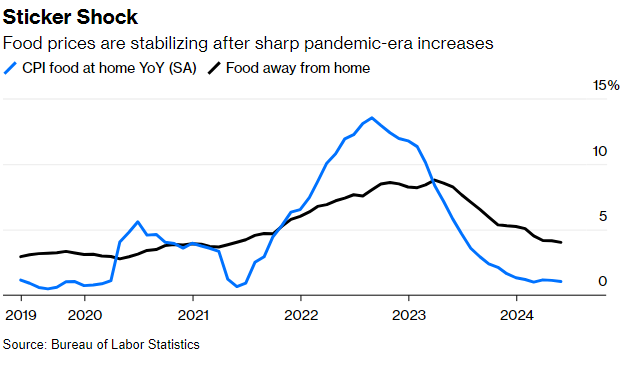

Consumers have delivered a message to consumer products companies: enough is enough with higher prices. To their credit, the companies seemed to have listened as evidenced by McDonald’s $5 value meal, Taco Bell’s $7 cravings box and budget breakfasts from Starbucks, the latter not a company with a history of cutting prices to woo customers. The food fight has begun and a return to normalcy for an industry defined by high volumes and low margins is at hand. “Food at home” inflation has fallen back to 1% on an annual basis from a high of 13.5% in 2022. Milk and seafood prices have been declining. In contrast, dining out expense inflation has been declining more slowly – but it is falling.

Chart 1

Restaurant companies are fighting for customers but the grocery store is also a fierce competitor. Consumer companies can no longer simply raise prices to grow. Shoppers will always find a better deal.

FOLLOWING UP…….

On a few comments we made last month regarding China’s economy and its fall from grace, we have found some interesting new information which only adds to our argument that China’s economy is not being effectively managed. China International Capital Corp (CICC), nicknamed the Morgan Stanley of China and founded 30 years ago, now has fully one third of its investment bankers as members of the Chinese Communist Party (CCP) when few during CICC’s early days would even admit to being a Party member. Its former hard charging ways mimicking Wall Street are gone. Party criticism of bankers’ hedonistic lifestyles are forcing banking execs to heed Xi’s call for “common prosperity”, which also exemplifies Xi’s growing control over China’s financial system. Gone are long workdays. Why? In April, CICC notified its bankers that their salaries would be cut by 25%. There were few bonuses given for work in 2023. Business is down. Morale is broken.

Chart 2

At Citic Securities, CICC’s main rival, about one third of the staff quit. China’s largest financial conglomerates have asked senior staff to forgo deferred bonuses and in some cases, return pay from previous years to comply with a pre-tax cap of $400,000. The world of finance operates like this in no other place in the world. As a result, the markets in China are not operating at potential and will not with the current rules in place. Without a financial system that can compete with Wall Street, China is relegating its economic advancement to a second tier. Markets in China will never be as deep, broad, or as well functioning as in the US to provide the necessary capital for China to grow to its ultimate potential. President Xi does not trust the markets made up of millions of investors, millions of voices. He trusts only himself – and therein lies the fundamental problem for China’s development.

SUMMING UP….

We have thought for some time that inflation was falling and still do – albeit with some “noise” in the monthly numbers. The re-emergence of value meals and widespread store “sales” to entice shoppers who might feel a bit stretched underscores the direction of inflation. With lower inflation, the Fed should be inclined to cut interest rates, which should support equity prices. Corporate earnings also are a very important support for stock prices. We have just started the earnings season for Q2 2024. So we’ll see shortly how strong this underpinning for stock market pricing is. Lastly, China has veered off the capitalist road pretty sharply. Politics, especially personality politics, has become too involved in the economy. This must change if China is to grow again as quickly as it had for years.

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed. The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results. We recommend that you compare our statement with the statement that you receive from your custodian. A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part II & Privacy Policy is available upon request or at www.baldwinmgt.com/disclosures.

Peter H. Havens, Chairman

Peter H. Havens, Chairman

Peter Havens founded Baldwin Investment Management, LLC in 1999 after serving as a member of the Board of Directors and Executive Vice President of The Bryn Mawr Trust Company. Previously he organized and operated the family office of Kewanee Enterprises. Peter received his B. A. from Harvard College and his M. B. A. from Columbia Business School. He serves as Chairman of the Lankenau Institute for Medical Research. He is a Board member of AAA Club Alliance, Main Line Health, The Lankenau Medical Center Foundation, and the former Vice Chairman of Main Line Health. He is a Trustee Emeritus at Ursinus College, Chairman Emeritus of the Board for the Independence Seaport Museum, former Trustee of the Leukemia Society of America, and a former board member of Main Line Health Realty and Lankenau Development Inc. He was also the Chairman of the Board of Petroferm, Inc. and a Board member of Nobel Learning Communities Inc