As we end 2023 and look forward to 2024, it appears to us that someone – or maybe a whole lot of “someones” – vigorously shook our snow globe. Snow is flying in every direction. Likewise, swirling geopolitical issues, overseas economic concerns and technological challenges are testing market commentators who are struggling to forecast which direction the markets will go. Nevertheless, let’s push ahead into 2024 and all that it holds for us.

In the New Year, there will be more than 70 elections from Mexico City to Moscow in countries which are home to approximately 4.2 billion people. One thing that all elections have in common is that they are expensive. The incumbents want to stay in office – so they “grease the skids” to make sure that government funds are spent to keep voters employed and happy. The challengers, despite lacking access to government coffers, raise and spend plenty of campaign money to support their platforms. Thus, more election-fueled money will be flowing through economies in 2024, involving a large part of the world.

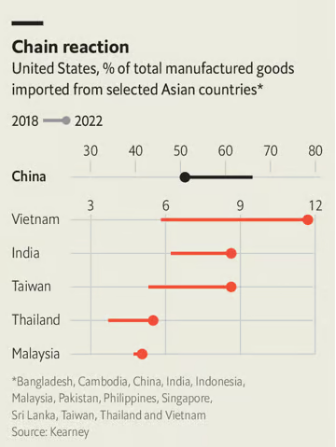

America will continue to have a strained, but hopefully a civil relationship with China. As Chinese political power has become more centralized in President Xi, Chinese decision making has also become more centralized in that very same person. This too often in history has resulted in flawed or static decision making. Examples of this sclerotic condition are the government’s severe approach to Covid, the near wiping out of the education industry, the bringing to heel of the Chinese technology industry, and the ongoing collapse of the real estate industry. In the words of the government, all these actions were taken to reform the industries under attack. The result has been a dramatic slowdown in Chinese economic growth, and capitalists from around the world, deeming China un-investable, have made Chinese markets cheap.

Chart 1

Companies have responded by taking steps to move production elsewhere (e.g., India, Vietnam, Malaysia, Mexico).

Chart 2

Tensions have risen across the Taiwan Straits as President Xi has again decided that a central part of his political legacy will be the re-unification of China with Taiwan. This is concerning for many reasons, one of which is it means that the economy will not run smoothly as it focuses on military matters. It also means that the U.S. needs to spend productive time and resources worrying about another Cold War with China vs. reaping the earlier days’ economic rewards of being a key partner with China and its formerly burgeoning economy. To counter this economic “soft patch”, the Chinese central government will have to support the economy.

TRANSITIONS

Artificial Intelligence (AI) really splashed onto the world scene in 2023. In the New Year, businesses will increasingly adopt AI in their business structures for fear of being left behind. There will assuredly be many more conversations and Congressional testimony about regulating this “genie”. Indeed, we believe that for our collective good, AI needs to be responsibly regulated. But the genie is out of the bottle and regulators will have trouble keeping up. Artificial intelligence can have leveraging influences in many aspects of our lives, enabling people to work far more efficiently and effectively, leading to major discoveries in almost every discipline more quickly that can enhance people’s lives now and into the future. But the “guard rails” need to be put up quickly or some bad actors could pollute this scientific breakthrough to the detriment of us all. We are not suggesting that all businesses will adopt AI in 2024. That is not the historical trajectory of technological adoption. A minority will be quick to adopt. Another group will be hesitant, and yet another will be wary for fear of what AI will do to their businesses. So, no doubt full adoption of AI will take time measured in years. But it should be remembered that 2023 saw the uptake of AI at a pace faster than any other technology introduced previously.

Speaking of transitions (another word for adoption), the green energy transition will continue to bump along. So far, there have been thousands of windmills placed on hilltops and anchored to ocean floors, and millions of solar panels deployed in deserts and on rooftops, all to generate “green” energy to supplant electricity once generated by coal, oil and natural gas. Big strides have been made to de-carbonize transportation, utilities and manufacturing. But as of today, many climate scientists fear that these efforts have not made enough of a dent to lessen the exhaust of carbon dioxide necessary to slow the rise of global temperatures.

Chart 3

The green transition will continue to move ahead – but only if it is supported by government subsidies. The economics of green energy are still not competitive enough with hydrocarbons. In 2023 several major offshore wind farms to be constructed were cancelled because of cost overruns and technological snafus. Green energy will occupy a greater share of the future energy mosaic that we all will use – but it will not happen as quickly as once supposed. Hydrocarbon use for generating power will be around for the foreseeable future.

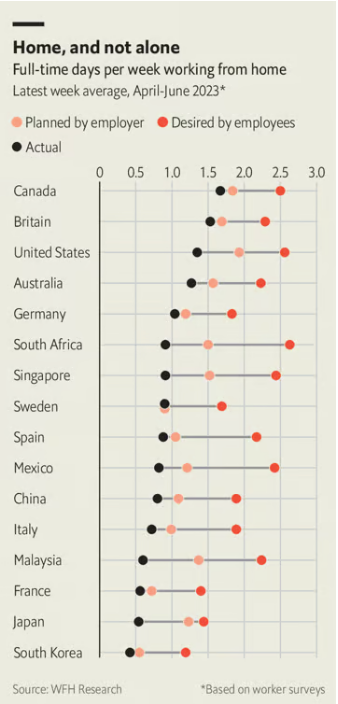

Moving on to the evolving workplace, work which had moved to a factory floor or an office building during various stages of the Industrial Revolution shifted once again back to the home because of the Covid pandemic. Office buildings emptied out and are still not back to occupancy levels extant pre-Covid.

Chart 4

Workers having become used to saving commuting time and gaining other conveniences have essentially said no to employers regarding coming back to the office full-time. With a perceived labor shortage, most employers have largely acceded to worker requests. But as labor markets soften a bit, more workers each day are being pressed to come back to the office. However, a gap remains. Landlords are being forced to improve their buildings’ amenities to make the workplace a more enjoyable experience. Some buildings are being converted to residential use. Other older, less attractive buildings are being torn down and taken out of the office building inventory. Solutions going forward will be expensive for office landlords.

After a couple of weeks of holiday celebration, we are all going to feel a bit pinched around our waists – wishing we had not eaten that last piece of pie. Further, no one likes to go on their obligatory post-holiday diet to reverse the aforementioned overindulgences. But in 2023, medical science brought to the market a new solution which prevents people from overeating because they feel full more quickly with less food. The drugs were originally developed for diabetics to help them control their HbA1c levels – i.e., blood sugar levels. Sales of these drugs have been booming and are projected to skyrocket in the coming years. Already competition from other drug companies with their competing drugs are heating up the race. With more competition, prices are dropping. Research is also expanding into other conditions like stroke, heart attack, sleep apnea, etc., and the results so far would indicate that these drugs have ameliorative effects on those major diseases. This is important because heretofore Medicare and insurance companies have not paid for weight loss drugs – but will pay for treatments to combat stroke and heart attacks. This ultimately will further enlarge the market for these groundbreaking drugs.

WILL AMERICA STICK A SOFT LANDING IN 2024?????

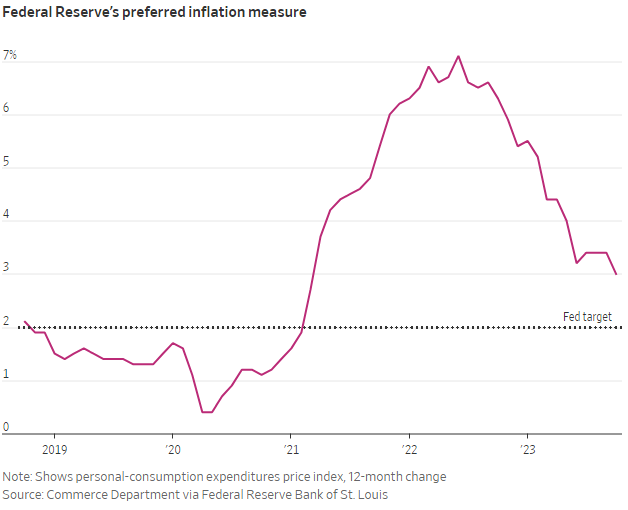

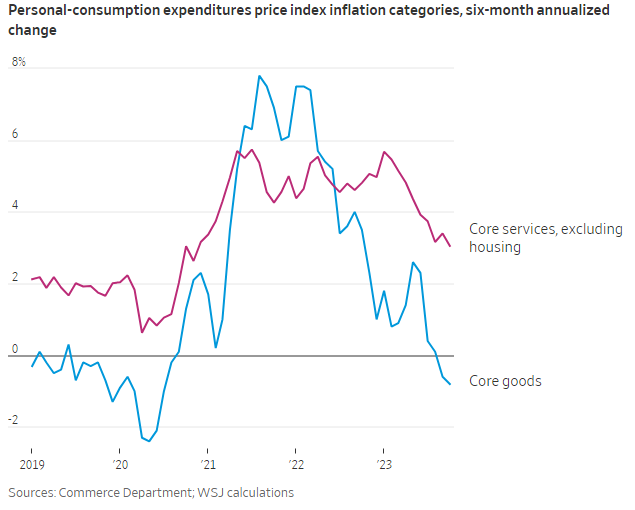

The odds clearly favor such an outcome more today than previously. Unemployment remains below 4% at 3.7% – very low historically. The ratio of job openings to the unemployed is essentially back to where it was pre-pandemic. So, labor markets are not as tight as they once were. Nevertheless, wages are growing faster than prices. Thus, workers are seeing real gains in their take home pay. Q3 economic growth came in at +4.9%, surprisingly strong, but not sustainable. Inflation has been receding for months. The Fed’s favorite measure of inflation, the core PCE (Personal Consumption Expenditure Index), which excludes volatile energy and food sub-indices, is around 3%, still a bit higher than the Fed’s 2% target year over year. But the Fed also looks at this measure on a latest three month annualized basis to get a sense of current trends. On that score the most recent reading came in at 2.16% – quite close to target and way down from last year. Following are two charts which demonstrate our falling inflation assertions. The second chart does not illustrate the 3-month trend, but rather the most recent 6-month trend, and the message is the same:

Chart 5

Chart 6

Cheered by encouraging inflation trends, Wall Street prognosticators are expecting that the Fed is nearly done/finished its interest rate hiking exercise. We would agree. In fact, we did not think that the last quarter point hike was necessary because previous interest rate hikes had not been fully felt so far in the U.S. economy due to inherent lags in their economic impact. Further, China for the past year has suffered from episodes of disinflation/deflation. As the U.S. still imports a great deal of product from China, no doubt America has been importing price reductions on many goods – which has and should continue to reduce inflationary pressures in the United States. In fact, the Fed after its December meeting clearly indicated that indeed interest rates are highly likely to be reduced in 2024, perhaps by 75 basis points. This should support U.S. equity and bond prices – as well as the American economy. Further, overseas markets could get a boost from rate reductions. As the U.S. is the world’s economic leader, what we do is usually mimicked elsewhere. So we could expect that other central banks will lower interest rates in concert with the U.S., but with a lag – thereby bolstering their economies and markets. As most foreign markets are decidedly cheaper than the U.S., there might well be a more pronounced “spring” in international markets’ prices given their relative values.

S&P 500 members’ earnings are slated to have a nice rise of about 12% in the coming year, supported by increased infrastructure spending, lower interest rates, and continued investment in technological advances like AI which will boost productivity. People are employed and are earning money, so they will continue to spend. Thus, we do not anticipate a recession in the U.S. in 2024.

POTENTIAL PROBLEMS TO PONDER…….

All the above is not to say that there are not problems out there which must be considered. Again, 2024 will be an election year. While politicians will no doubt be keeping their eyes on the “prize”, there is other work that needs to get done like getting budgets passed – so governments can function. The Ukraine/Russian war also distracts. Important supply lines for European energy have been recast so there is no longer a worry about supplies being cut off- in fact, energy prices have fallen. Nevertheless, this war has upended numerous aspects of European life and since we do not know its conclusion yet, it is a risk. Very much the same can be said about the fight between Israel and Hamas. Already it has gone on for more than two months and is centered in an area of the world infamous for battles getting out of hand and having unpleasant repercussions elsewhere. So far, nasty side effects outside of the epicenter have been few – and we pray that continues to be the case. Elsewhere, Chinese regional and local debt could spiral out of control, damaging the overall economy. We think the situation is being well monitored and the central government’s shoulder is being put to the wheel. This also bears watching. China is still grumbling about Taiwan and the latter will have an important Presidential election in 2024. However, we believe that China’s economic problems are currently occupying President Xi and his colleagues. A war with a well-defended adversary one-hundred miles off the Chinese coast is probably not a fight President Xi wants to have right now. Further, China has become so much of a bully in its foreign policy that it has irritated many of its neighbors surrounding the South China Sea (think Philippines, Vietnam, Malaysia, etc.). Thus, Taiwan might have quite a few friends to stand by its side in a spat with the mainland. But we must be aware.

AND SO…….

A year ago, we did not believe that the U.S. would go into recession. With the American consumer representing approximately 70% of the U.S. economy, we thought that employment was too high and the consumer’s balance sheet was too strong for the American economy to “tank”. We continue to think that a recession is not in the cards in 2024 because while U.S. consumers have spent a good part of their pandemic savings, they remain well-employed and have solid personal balance sheets. Further, there will be more capital investment in 2024 from companies and the U.S. government and let’s not forget the additional political spending that will occur through the year. Lower interest rates will be helpful to business and investor alike. Internationally cheap stocks may get some wind at their backs with a lower dollar after interest rates are reduced. There are issues in Eastern Europe, the Middle East and on either side of the Taiwan Straits that investors must watch closely. So far none of these has become so great a worry that it has dragged down the markets. We believe that these difficulties will remain “ring-fenced” and look forward to another good year in various markets around the globe.

A FINAL THOUGHT…

The opinions expressed in this Commentary are those of Baldwin Investment Management, LLC. These views are subject to change at any time based on market and other conditions, and no forecasts can be guaranteed. The reported numbers enclosed are derived from sources believed to be reliable. However, we cannot guarantee their accuracy. Past performance does not guarantee future results.

We recommend that you compare our statement with the statement that you receive from your custodian. A list of our Proxy voting procedures is available upon request. A current copy of our ADV Part II & Privacy Policy is available upon request or at www.baldwinmgt.com/disclosures.